„Germany 21: Regionaler Büromarktindex“ (Quelle: Corpus Sireo 2017)

Shortage of Products driving office rents at A- and B-Locations: The CORPUS SIREO “Regional Office Index” study confirms the continuing positive growth of German A- and B-locations on the office markets. In the 19 B-locations studied, asking rents were €8.73 per square metre at the end of the first half of 2017. This signifies an increase of 1.9% compared with the end of 2016. In the top seven cities, asking office rents increased by 2.1% to €13.97 per square metre in the same time period.

The study is carried out by CORPUS SIREO, the German property subsidiary of Swiss Life Asset Managers, and the Bonn-based research institute empirica. Focal city Freiburg Germany’s most expensive B-Location. The full report is available as a free download at corpus-sireo.com

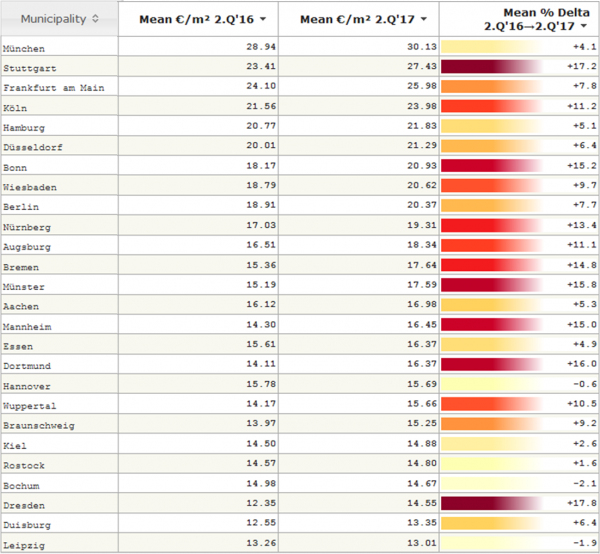

Since our latest rent overview in February 2017, Munich has exceeded the 30 Euro per m² threshold and Stuttgart has pushed Frankfurt from the second to the third place – with a rent of 27.43 € per m². Compared to the second quarter 2016, Stuttgart is also the A-City with the highest rent increase. Since then, only Dresden has seen a (relatively) higher increase. The analysed advertisements are furnished, for temporary use and the rates include ancillary costs.

Gross rents for temporary accommodation (1 & 2 room flat adverts – 2016/2017). Source: empirica-systems market data base 2017

The total rent in the German A-Cities varies from 1167€ per month in Munich, 992€ in Frankfurt, 968€ in Stuttgart, 902€ in Cologne, 883€ in Dusseldorf, to 820€ in Berlin and 794€ in Hamburg.

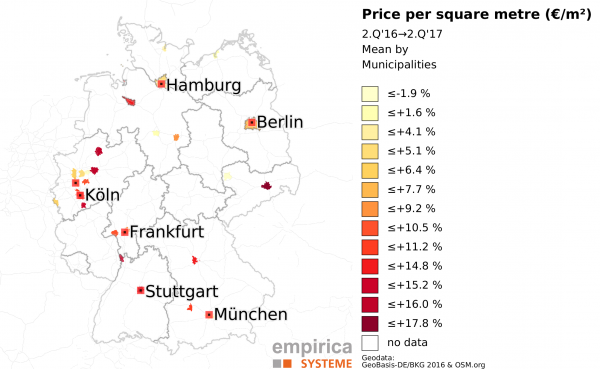

Gross rent per square metre for temporary accommodation (€/m²) Delta 2.Q’16→2.Q’17. Source: empirica-systems market data base 2017

Mit Stichtag 09.04.2017 stehen die aktuellen Immobilienmarktdaten für das I. Quartal 2017 sowie ein Update der Analyst-Software für Sie bereit.

Aktuelle Immobilienmarktdaten Top-7

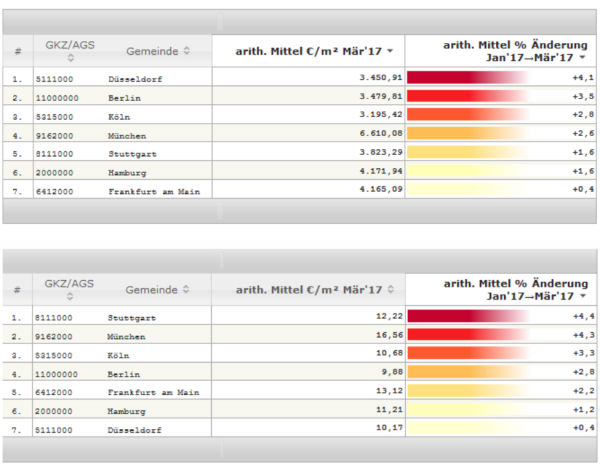

Zwar findet das offizielle Update der neuen Immobilienmarktdaten aus betrieblichen Gründen erst am Wochenende statt, wir möchten auf diesem Wege aber bereits jetzt ein paar Einblicke in aktuelle Preis- und Mietentwicklungen des deutschen Wohnimmobilienmarktes geben: Die höchsten Preissteigerungen (kein Erstbezug, kein Neubau) zwischen Januar und März 2017 verzeichnen wir in Düsseldorf, gefolgt von Berlin, Köln und München, während im Mietsegment Stuttgart das Feld vor München, Köln und Berlin anführt.

Preise (oben) und Mieten (unten) der Top 7 Märkte im März 2017, Entwicklung Jan’17 bis Mär’17 (Kein Erstbezug, kein Neubau, Stand: 4’2017, Quelle: empirica-systeme Marktdatenbank)

Corpus Sireo hat die 12. Auflage des regionalen Büromarktindex “Germany 21” vorgestellt. Da das Angebot an Spitzenobjekten in den Top-7-Standorten zunehmend knapper wird, werden regionale Büromärkte als Alternativstandorte demnach immer wichtiger.

Deckblatt “Germany 21: Regionaler Büromarktindex” (Quelle: Corpus Sireo 2017)

Der „GERMANY 21: Regionaler Büromarktindex“ zeigt, dass sich in den letzten Jahren neben den Top-7-Standorten auch die 14 untersuchten mittelgroßen Büromärkte (Aachen, Bonn, Bremen, Dortmund, Dresden, Essen, Hannover, Karlsruhe, Leipzig, Mainz, Mannheim, Münster, Nürnberg, Wiesbaden) gut entwickelt haben. Es wird erwartet, dass die Mieten in diesen Märkten künftig stabil bleiben bzw. leicht steigen. Damit bieten sie solide Anlagepotenziale für Immobilieninvestoren. Im Gegensatz zu den umkämpften Investmentmärkten der Metropolen ergeben sich hier nach wie vor attraktive Einstiegspreise und nachhaltig gute Renditeperspektiven. Fokusstadt der 9. Auflage des Berichts ist Mannheim

For those who are interested in German market for micro-living and student housing, we have taken a look into our data to figure out some facts which may improve the understanding of the German student housing market.

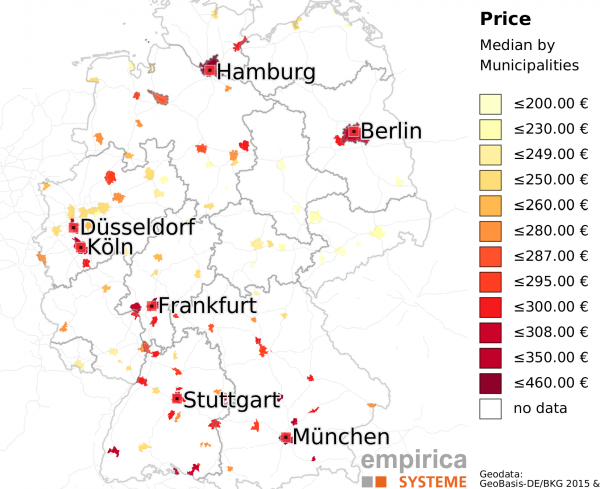

Total median rents of shared-flat living offers 2016 (only cities with more than 200 offers, source geodata: GeoBasis-DE/BKG 2015 & OSM)

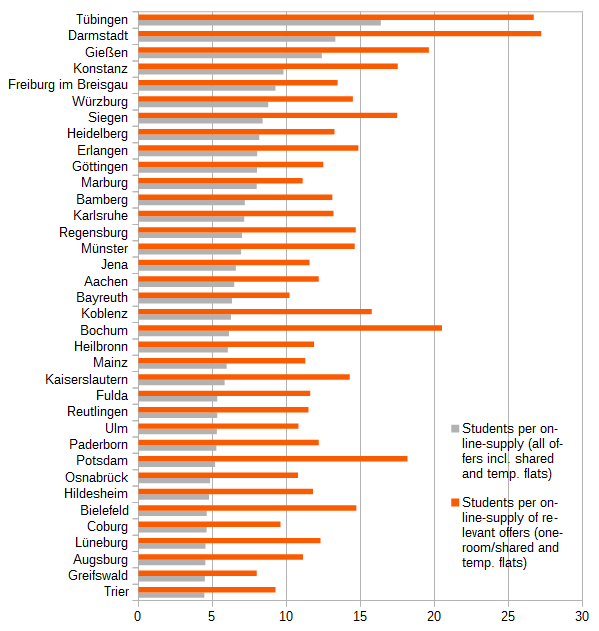

Identifying tense student markets

The university cities show the highest student demand excess, measured by students per online ads [(students – students in residence halls)/online offers)] , especially in student compatible sub-markets (‘one-room-flats’, ‘shared flats’ and ‘temporary living offers’). In Tübingen and Darmstadt there are more than 25 students for each student compatible residence offer.

Student demand per (online) supply 2016

Shared flats are an essential sub-market

We found out, that the market segment ‘shared flats’ is essential and valuable in context of analysing student housing markets as well as for micro-living issues.

High market shares of ‘shared flat offers’ indicate student markets, as well as markets with high demand for ‘one-room-flats’ and ‘micro-apartments’. Rates for ‘shared flats’ also indicate accepted market rents, their upper percentiles show a critical willingness to pay and their spatial distribution indicates student hotspots. Despite these aspects the segment is hardly under investigation.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.